Do credit markets price scope 3 emissions?

Do credit markets price scope 3 emissions?

Reporting on greenhouse gas emissions has historically been focussed on scope 1 and 2 emissions. But regulators and voluntary disclosure standards increasingly focus on scope 3 emissions that make up the majority of all emissions. With scope 3 emissions being a relatively new concept, one has to wonder if credit markets are pricing these risks or if they largely ignore them.

One of the problems of ESG indices is that they typically focus on scope 1 and 2 greenhouse gas emissions to decide on the companies that are included in an index. However, once emissions are broadened to scope 3 emissions, then the emissions advantage of ESG indices disappears quickly, as I have discussed here.

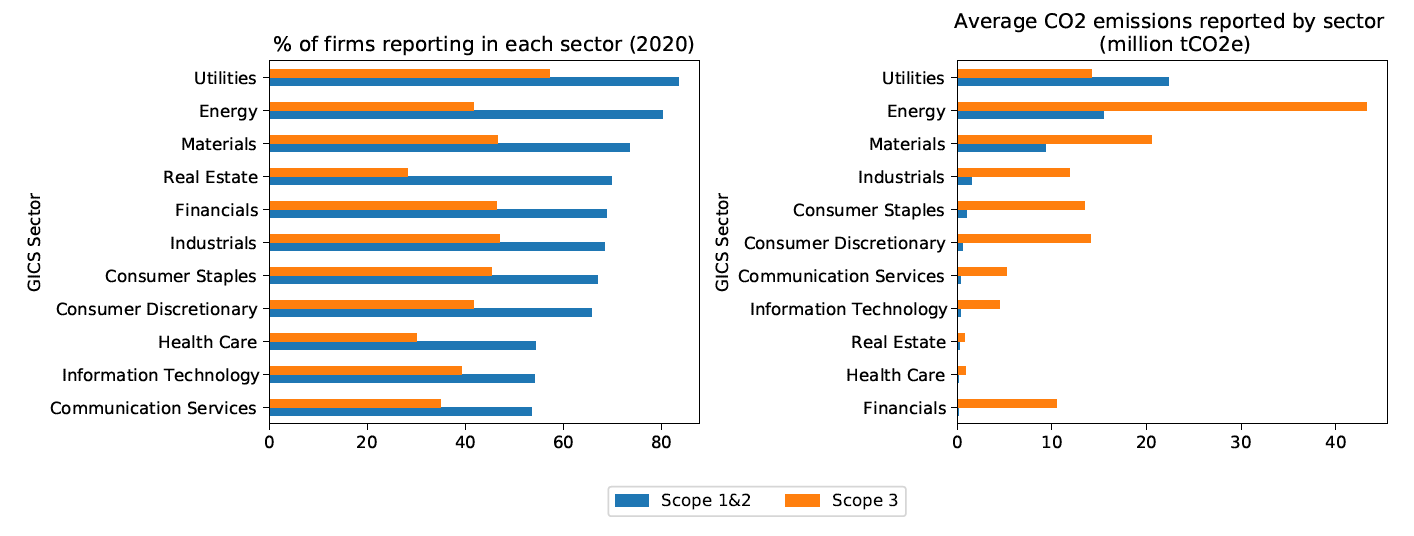

Similarly, if one looks at the reported emissions of different sectors, then the differences between sectors in scope 1 and 2 emissions are large, but they are significantly smaller when scope 3 emissions are taken into account. All of a sudden, big polluters like energy, materials and utilities have higher but not much higher emissions than other sectors.

Emissions reporting and emissions intensity by sector

Source: Panjwani et al. (2022)

Ahyan Panjwani and his colleagues examined the 2,720 companies in the MSCI All Countries World Index and their greenhouse gas emissions. They then looked at the cost of debt of these companies and tried to assess if companies with comparable financial leverage, profitability, etc. pay higher interest rates on their debt if they have higher emissions. Their findings show that scope 3 emissions are so far only partially priced in credit markets. Companies that disclose their scope 3 emissions on average get a reduction in the cost of debt of 20bps. Hence there is something like a transparency bonus. However, the researchers could not find any impact of the size of scope 3 emissions on the cost of debt. In other words, big polluters were not penalised in the form of higher costs of debt.

If you ask me, that is something that is about to change in the future. As scope 3 data becomes more widely available, I think lenders and investors alike will gradually incorporate these emissions into their assessments of the climate risks of an issuer. As lenders shift from scope 1 and 2 to scope 1-3, this risk premium for polluters will emerge and force companies to reduce not just their scope 1 and 2 emissions but their total greenhouse gas footprint.

In the meantime, issuers can get a discount on their cost of debt by simply being more transparent about their scope 3 emissions…