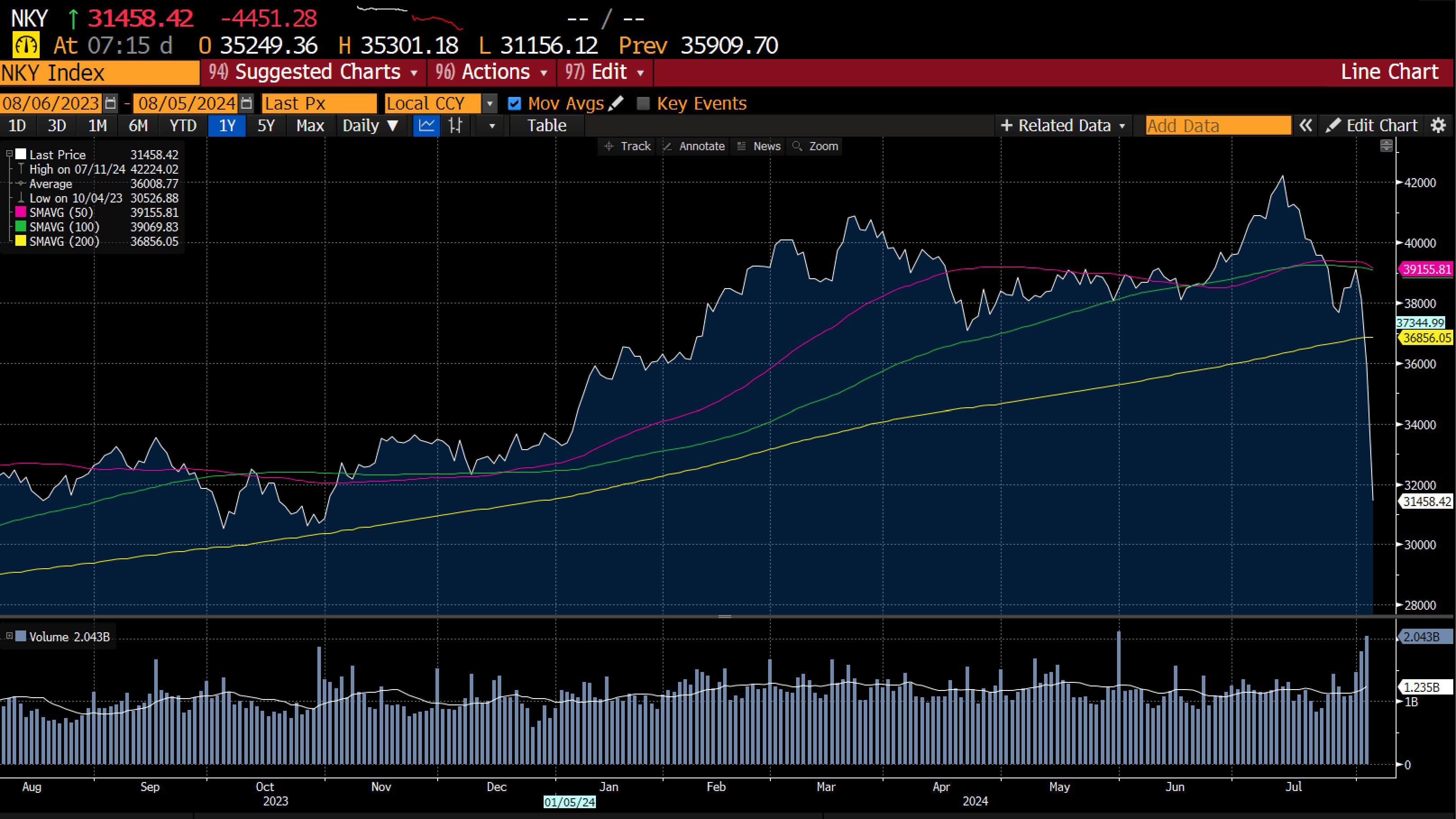

For a long time I have said the BOJ was the most powerful central bank in the world, and we have prove of it today. Raising interest rates, and reducing QE, has turned Nikkei from an up trending market to bear market very quickly.

A collapsing Nikkei tends to be seen as a indicator of incipient economic doom. But even with the moves today, the Japanese 30 year still seems to be in an uptrend.

As is the relative Japanese bank trade.

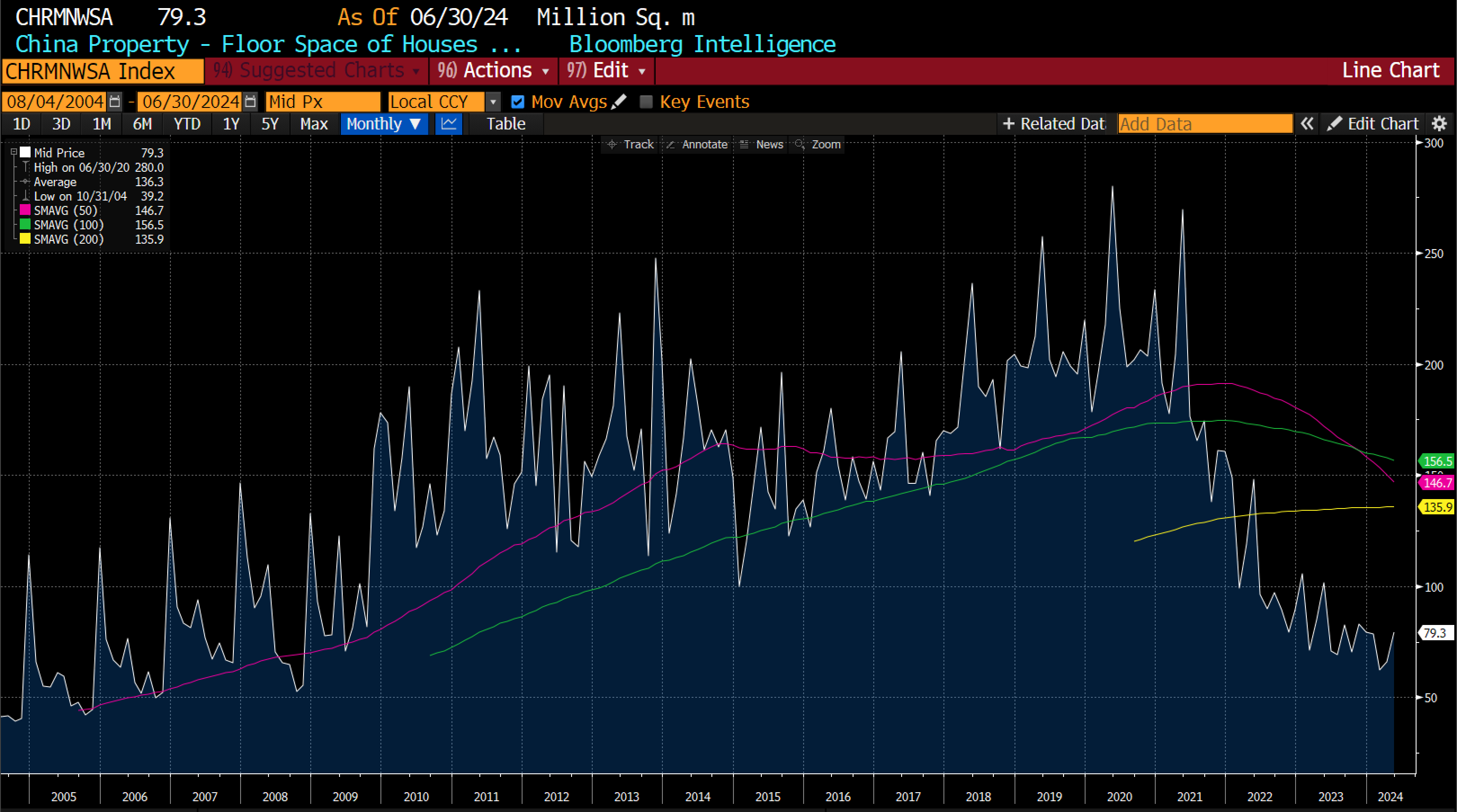

The problem with the deflation story is that it that bond yields have already proven themselves to be a policy story more than a macro story. Do you remember when every economist and hedge fund manager was telling you that the unwinding of the Chinese property bubble would be the GFC on steroids. Chinese property developers have gone bust in droves, and property starts in China has collapsed. And yet US bond yields have remained fairly high, and JGBs remain in bear market.

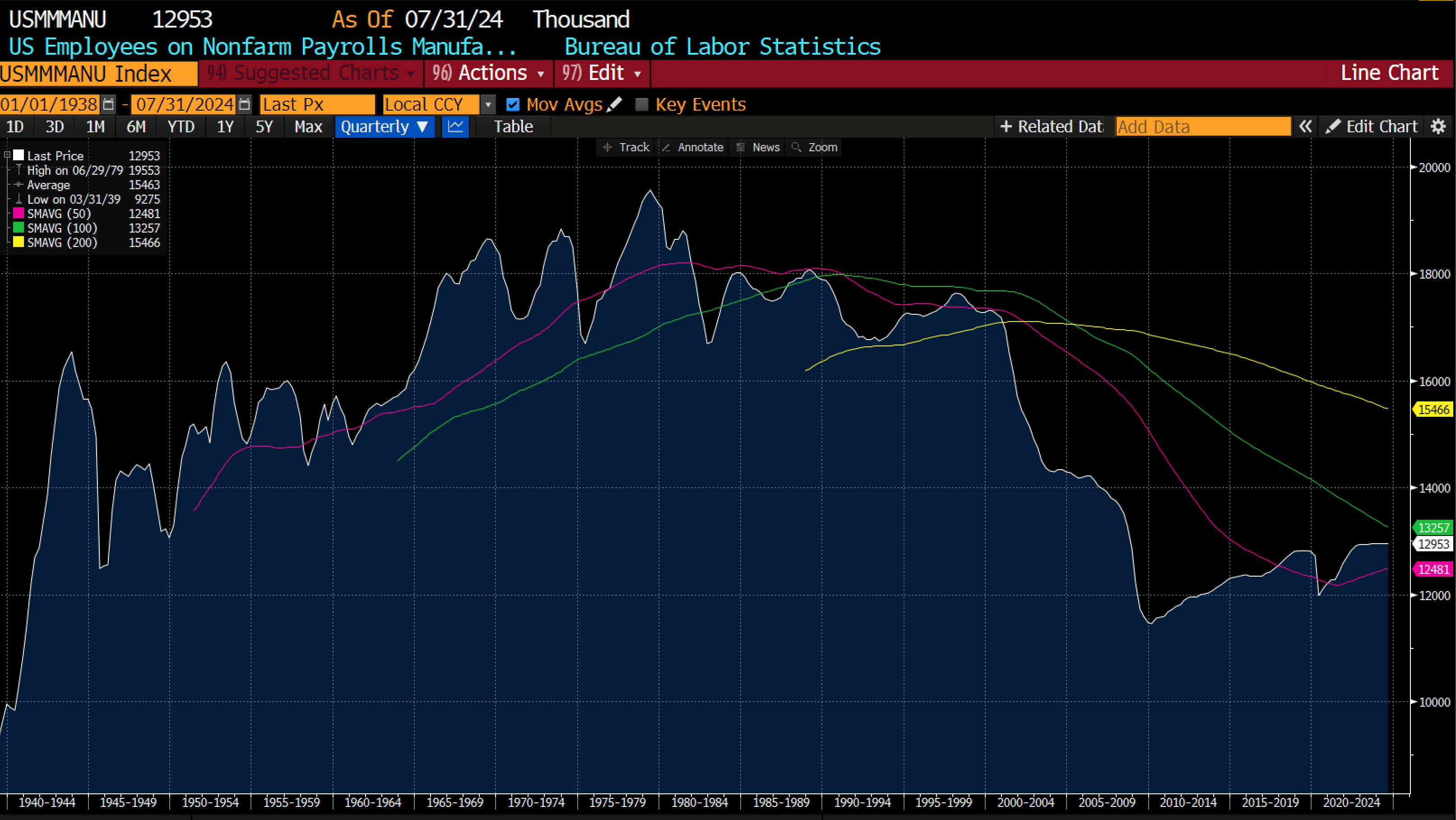

Looking at US policy going forwards, both Trump and Harris I think would like to restore US manufacturing to its former glory. Using non-farm payroll data, we can see how much more employment would need to rise in this sector. The US lost 6mn manufacturing jobs from 2000. Could policy restore this? I think they are going to try - and it will not be deflationary!

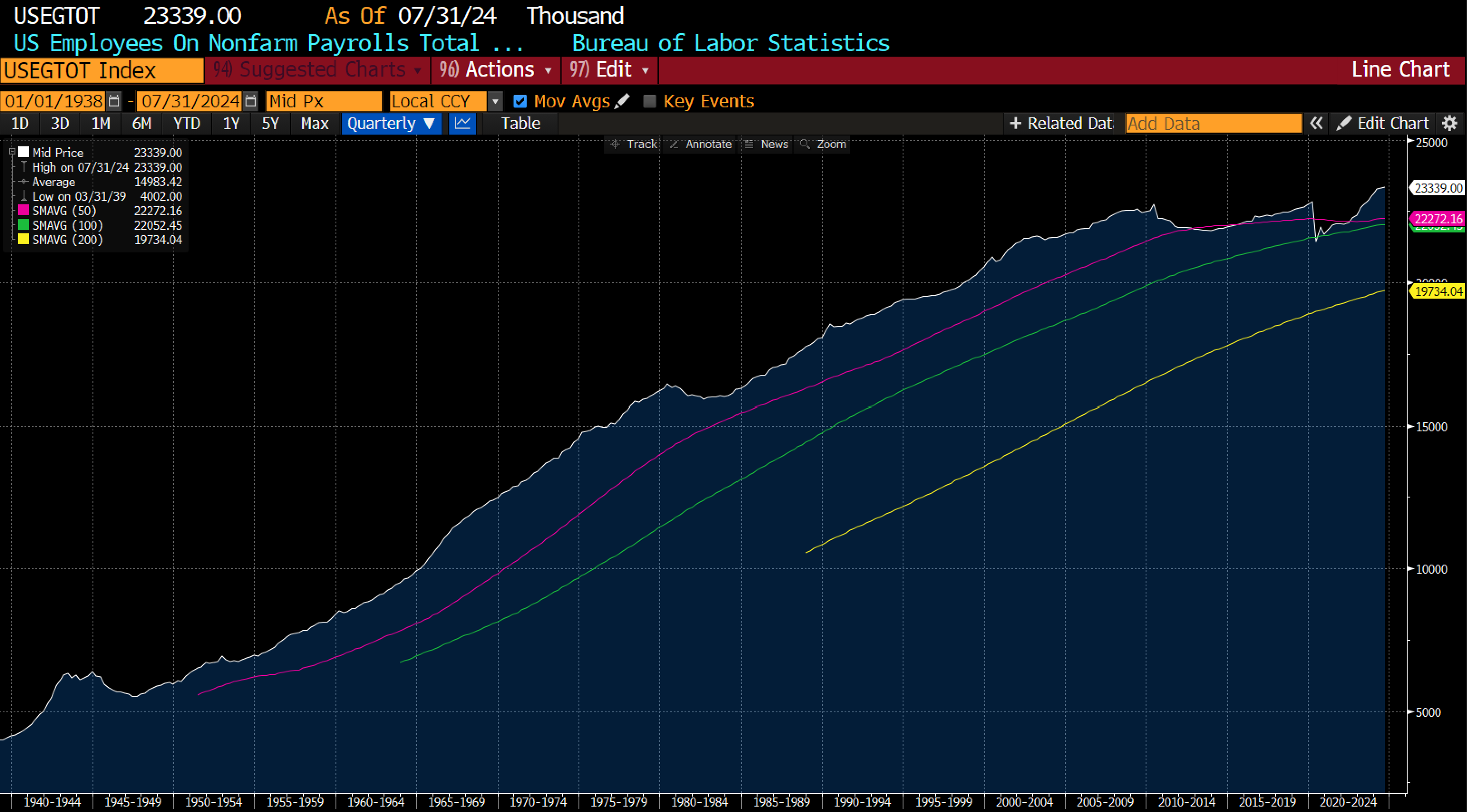

Curiously, the number of US government employees has recently risen to new highs, after a long period of stagnation.

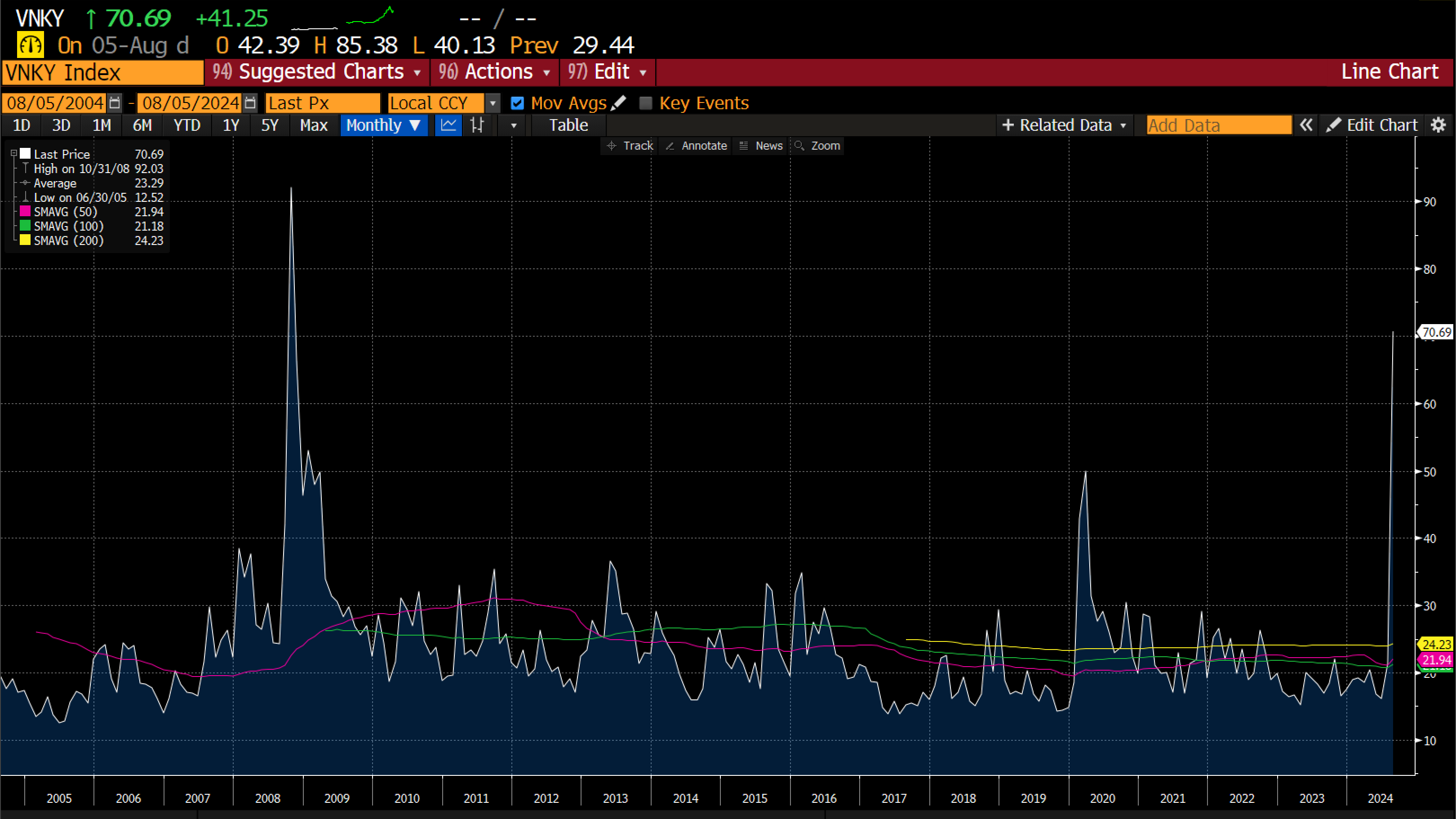

Hopefully this helps you understand where I am coming from. Deflation had little to do with economics, and more to do with government policy. Inflation has little to do with economics and more to do with government policy. For me, policy is inflationary. So why have markets moved so violently? Well I have to go back to the way clearinghouses price risk - which is backward looking. So even though the BOJ has been talking about raising rates, clearinghouses not have anticipated any volatility until it actually happens. Once volatility spikes, THEN they ask for more initial margin, which then causes more volatility and so on so forth. As I pointed out, clearinghouses create more financial volatility, and likely bankruptcy. Their only “benefit” is that governments can bail out market via clearinghouses rather than banks. The Nikkei VIX chart give you a good idea of how bad they are at pricing risk. Nikkei vol trended higher into the GFC, but todays 70 print came from nowhere. Margin call is the answer.

I ask myself, is the political will there to create unemployment to defeat inflation? I don’t think so. The BOJ is reacting to this change very slowly, and leveraged players are going to go to the wall, but I don’t think we are going to see austerity anytime soon. The stupidness of clearinghouses is going to let you get in on inflation trades at good levels I think.

GLD/TLT still looks good to me.

if anything, I suspect that policy reactions to this move are going to drive even more inflation

With property prices already rising - interest rate cuts are hard to see

This is the main hurdle, the barriers to increasing housing supply in English-speaking countries are just too high!

it seems policymakers have made themselves quite an uncomfortable bed

Policymakers follow.what voters want....

Completely agree Russell.

How can you claim that the BOJ is the most powerful CB in the world if Japan lost the war and remains occupied? Clearly the BOJ does whatever it is told to do by outside forces. Your clarification on this would be appreciated.

I did skip a few steps. Japan uniquely among nations, run a capital account surplus at the government, corporate and household level. By that I mean, it invests more in the rest of the world, than the rest of the world invests in Japan. The AVERAGE Japanese person has around USD250,000 saved, versus the average American who would be in debt. So Japanese savings are a massive force in international finance. For years GS used SMFG balance sheet, and Japanese government is the largest holder of treasuries. So when I say the BOJ is the most powerful CB - what I mean is that changes in policy at the BOJ causes changes in the biggest single savings pot in the world -hence when BOJ has tightened rates since the 1990s, financial crisis has followed. Hope that makes sense. Russell

Thank you for elucidating your thought process—although I still think BOJ policy plays second fiddle to the Fed, ECB, and perhaps now even the PBOC. Anyway, I hope you're enjoying the extra volatility so far this month!

What do you think about central bank liquidity peaking in April as the initial spur to the down trend in equities which is then made worse by CH rules? Heard Matt King talking about this on Odd Lots.

Govt policy should dominate CB liquidity. So withdrawing liquidity cause volaitily but no change economically

Hi Russell - what is the relative Japanese bank index

Is it Topix Banks vs Topix?

Topix bank v topix

great post RC - are there any data sources you use to monitor clearing house margin amounts/rates for various products?

Vix tends to be the best visible measure

The clearinghouse aspect of the volatility machine is not something I read elsewhere, but it makes a lot of sense. So do you think the market volatility still has some ways to go until something “breaks”?

In the last few years when clearinghouse "rules" threaten to break the market-policy makers have preferred to break the rules...

Thank you. Btw which BBG ticker do you use to track the movement of BOJ assets size ?

Toys3020