All you need to know about Employee Stock Option Pool (ESOP) Part #2

All you need to know about Employee Stock Option Pool (ESOP) Part #2

Good Morning on this Monday 🚀,

This weekly tech newsletter will help you to start your week right with topics around technology, founders’ infrastructure, and more - do not miss out and subscribe here:

After having laid the foundation for the general structure of ESOPs in last week’s piece, we will dive one layer deeper today, by focusing on the strike price & vesting, what implication an ESOP top-up has as well as some housekeeping. (PS: If you have missed Part #1 of the ESOP Guide, I strongly recommend you read this, before jumping into Part#2, considering Part#2 will build up on the first part)

Previously on…

Getting shortly back to the important topic of ESOPs being carved out based on the companies’ pre-money or post-money valuation.

Remember, including the ESOP into the post-money valuation is more founder-friendly, given the dilution impact will be spread among founders, existing investors, and most importantly new investors during the round. However, the current market standard in Europe is the inclusion of ESOP into the pre-money valuation. This will lead, to an effective reduction of the pre-money valuation (by the volume of the ESOP) - in other words, it is effectively decreasing the share price offered by the investor/s.

Founders need to understand this “shuffling” of ESOP because this can cause various bad surprises and/or constraints with new investors if this mechanic is not fully understood.

This phenomenon, when it comes to the creation of an ESOP during a round is called “Option Pool Shuffle” as famously established by Babak Nivi (Founder of Angellist)

🔀 Option Pool Shuffle

“Option Pool Shuffle is mainly a term for the negotiations surrounding the size of the ESOP.”

The shuffling of ESOP has not only an impact on the present round but also on the future rounds to come. Founders should have their rationale and standing point on those potential misadventure factors for future rounds when discussing with investors about the ESOP size and where to “shuffle” the ESOP.

Founders should be worrying about contributing too much to the ESOP pool and create a “larger than necessary” pool from the get-go. If the newly established ESOP pool will be not fully allocated for the next round, further disadvantages for founders will be unlocked:

Unallocated stock options will be rolled over: This means if the ESOP size needs to be increased at the next funding round, the investors from the previous round would not need to be diluted as much. In other words, the founders’ excess dilution carries over.

Canceling of unallocated and unvested options during a trade sale: If the company is sold before the next round (unlikely for seed companies, though), unissued and unvested options will be canceled, creating a form of “reverse dilution.” In other words, when you exit, some of your pre-money valuations will be spread across all shareholders.

How can founders prevent this from happening?

Fred Wilson (Founder of Union Square Ventures) highly recommends founders create/have a hiring plan (as already mentioned in Part#1), to fund the company’s planned hiring and retention until the next funding round. Headcount-based hiring plan with expected options against each hire combined with a retention plan of current employees who will expect to receive additional options.

Bottom line, Use a hiring plan to justify a small option pool, increase your share price, and increase your effective valuation.

How can founders prevent this from happening?

Fred Wilson (Founder of Union Square Ventures) highly recommends founders create/have a hiring plan (as already mentioned in Part#1), to fund the company’s planned hiring and retention until the next funding round. Headcount-based hiring plan with expected options against each hire combined with a retention plan of current employees who will expect to receive additional options.

Bottom line, Use a hiring plan to justify a small option pool, increase your share price, and increase your effective valuation.

🔝 Top up

The ESOP pool is typically increased (“topped up”) at each funding round. Practically, in each funding round, a “new” ESOP is created, representing the top-up amount suggested by the investor. The ESOP pool top-up is typically shared between all existing shareholders, translating into shuffling the top-up into the pre-money valuation.

After carving out the ESOP on your cap table during the funding round, you eventually need to create your legal structure for your ESOP plan with your legal advisor, which includes two important frameworks :

Vesting Schedule ⌛️

Strike Price ⚡️

Below, you can find an outline, seen in the European & Nordic ecosystem, hence can be considered “standard practice”.

⌛️ Vesting Schedule

Stock options should incentives employees in the long-term and should compensate for the lack of cash reserves of early-stage companies, as outlined in Part#1. Therefore, it is general practice to vest the granted stock options over a certain period, to keep the motivation high throughout a larger timeframe, instead of enabling employees to convert their granted stock options into shares immediately, which would have a reverse impact on the aimed retention rate.

In addition, if an employee leaves the company before they are fully vested, the unvested portion is canceled and returns to the unallocated ESOP pool. However, depending on the circumstances of the “leaving” employee, certain jurisdictions on so-called “Good leaver” and “Bad leaver” will be applied.

Traditionally, in Europe we see a four-year vesting schedule with a one-year cliff, for seed companies:

Traditional Vesting period - Still the norm?

As mentioned, a four-year period vesting schedule is pretty much seen as standard across Europe, also regardless of role or seniority. Throughout the four-year period, stock options vesting generally linear (25% each year), starting immediately after the end of the cliff. Depending on the jurisdiction and taxation, vesting is conducted mostly monthly but can be done quarterly or annually as well.

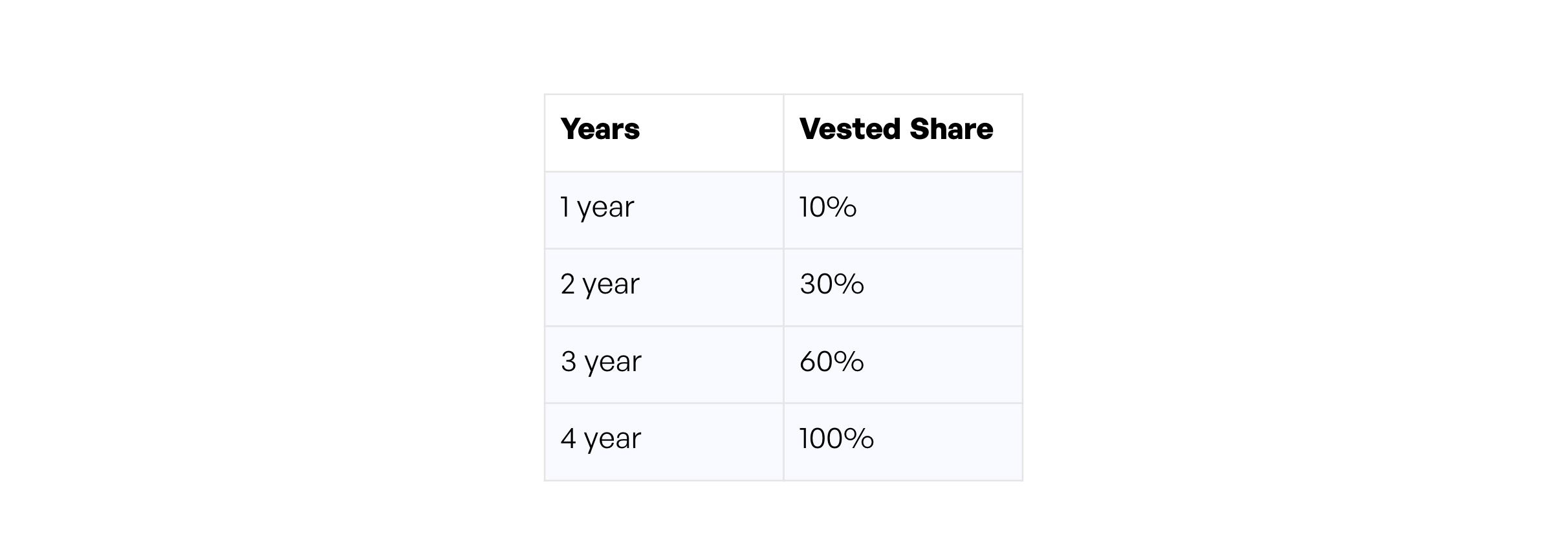

However, is this still the norm and represents the current market? This is an open question and highly debatable. But in recent years, large tech companies such as Amazon or Snap have used a new vesting schedule, called “Back Loaded Vesting” which gives employees smaller portions of shares in the initial years, and larger towards the end of their 4-year period. This structure is used much more as a way of retaining high-caliber talent, than actually hiring talent. An example vesting schedule could look like this:

I am surprised that we have not seen a wider introduction of a back-loaded vesting schedule. Considering the ongoing war for talents, this could be a mechanical solution to encourage a company’s high-caliber talent to remain at the company, to maximize their vesting, rather than leaving for a new adventure. I honestly would like to see more founders taking on back-loaded vesting schedules!

Cliff

Generally, a “Cliff” describes the timeframe throughout which no stock options are vested. Only after the respective timeframe of the cliff, do the stock options start to vest. This framework should protect companies from mis-hires and avoid the resulting dilution. Especially, for fast-growing early-stage companies, which usually have a large turnover & churn of talent.

⚡️ Strike Price

This is the share price that the employee has to pay if exercising the stock option and converting to a share. It is also referred to as the exercise price or option price.

The strike price is still one of the most discussed frameworks across early-stage companies, considering its tax impact on employees as well as the complexity in orchestrating your cap-table if issuing a large number of different strike prices.

But the most important question among early-stage founders is - How is the strike price determined within the ESOP? There is no straight line answer to this question, considering different jurisdictions from country to country in Europe. In Germany for instance, strike prices are set at the valuation of the last round. However, across the Nordics, the strike price can be set at any price, with the nominal value as the legally lowest price (defined as the company’s share capital divided by the outstanding shares).

In contrast, in the US (as well as for every operating European subsidiary) the companies can not allocate stock options below their fair market value (FMV) according to the IRC 409A regulation, which in turn requires the company to exercise a so-called “409A Valuation” to determine the companies fair market value. I will not deep dive into those mechanics, considering a large number of interesting articles out there:

An additional question, founders tend to ask is about setting the right strike price. Again, there is no perfect answer to the question, but clear guidance in my opinion, on what founders should consider when ultimately setting the strike price.

Some could argue, that a high strike price could lead to non-conversion of shares or a larger ask absolute number of options by the employee, but that solely leads to a misalignment between founders & employees, as far as i am concerned. Also considering that employees will convert their stock options into common shares, rather than preferred shares, hence less valuable. Therefore, the employee almost has no financial benefit.

I believe setting the strike price at a discount could turn more favorable for founders, due to the increased financial benefit, which in turn will have an impact on both retention rate and motivation, but also would protect employees for down-rounds marking the company at a lower valuation, than its last funding round. Meaning that the options are still valuable, for employees. The latter factor should especially in the current market environment not be neglected.

See you next Monday 🦄

PS: Feel free to share this post with whomever you think is helpful!